How Do You Get Pre-Approved for a Mortgage in Katy, TX?

Quick Answer

To get pre-approved for a mortgage in Katy, TX, you'll choose a lender, submit income and asset documents (pay stubs, W-2s or tax returns, bank statements, ID), authorize a credit check, and receive a pre-approval letter stating how much you're qualified to borrow. Most Katy buyers can get a pre-approval letter in 24–72 hours once documents are submitted. As of mid-2026, 30-year fixed mortgage rates are averaging in the mid-6% range, and Fort Bend and Harris County (which cover Katy) fall under the standard 2026 FHA loan limit of $541,287 for a single-family home, with a Texas conforming loan limit of $832,750.

Key Takeaways

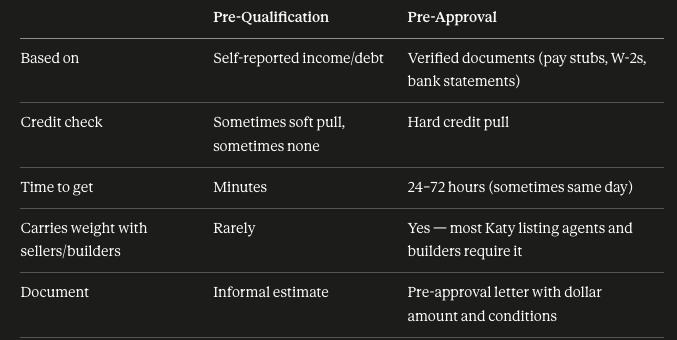

Pre-approval is different from pre-qualification — pre-approval requires document verification and a credit pull, and it's what sellers and builders in Katy actually take seriously.

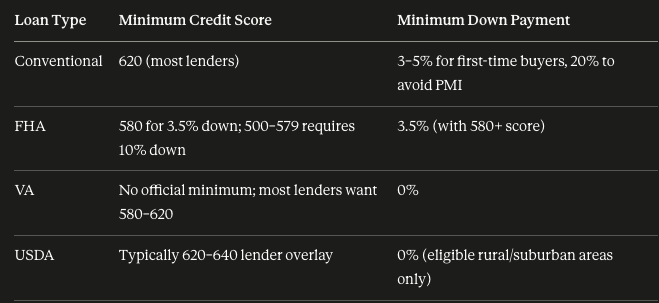

You'll generally need a minimum credit score of 580 for FHA (3.5% down) or 620+ for most conventional loans; VA loans have no set minimum but lenders often look for 580–620.

Debt-to-income (DTI) ratio matters as much as credit score — most lenders want your total monthly debts, including the new mortgage, at or below 43–50% of gross monthly income, depending on the loan program.

Texas offers real down payment help — programs through the Texas State Affordable Housing Corporation (TSAHC) can provide up to 5% of your loan amount toward a down payment or closing costs.

In Katy's new-construction-heavy market, builders often require a pre-approval letter before you can even lock in a lot or design center appointment — so this step often comes before house-hunting, not after.

Pre-approval letters typically expire in 60–90 days, so timing matters if you're not ready to write an offer yet.

Pre-Approval vs. Pre-Qualification: What's the Difference?

Quick answer: Pre-qualification is a quick, informal estimate based on what you tell a lender. Pre-approval is a verified, underwritten commitment based on what you prove — documents, credit pull, and often a conditional underwriting review.

In Katy's market, especially in master-planned communities working with builders like Perry Homes, David Weekley, or Highland Homes, a pre-qualification letter usually isn't enough to reserve a lot or move forward at the design center. Builders and sellers want the verified version.

Why Get Pre-Approved Before You Shop for a Katy Home?

Getting pre-approved first isn't just paperwork — it changes how you shop.

You know your real budget. Katy's home prices vary widely by area. Citywide, the median sale price has been running around $350,000, while newer, higher-end sections of the 77494 zip code (Cinco Ranch, Cross Creek Ranch, Elyson) often run closer to $460,000–$500,000. Pre-approval tells you which of those markets actually fits your budget before you fall in love with a floor plan.

Your offer gets taken seriously. In a market where homes are receiving multiple offers or sitting slightly longer (Katy's average days-on-market has been trending up), a pre-approval letter signals to sellers and their agents that your financing is real.

You catch problems early. If there's a credit report error, a debt you forgot about, or an income documentation issue, you want to find that out before you're under contract with a 10-day option period ticking, not after.

New construction requires it. Builders in Katy frequently require pre-approval — sometimes with their preferred/in-house lender — before you can select a lot, lock a price, or start design center selections.

What Documents Do You Need for Pre-Approval?

Have these ready before you contact a lender — it's the single biggest thing that speeds up the process:

Income Documentation

Last 30 days of pay stubs

W-2s from the last two years

Federal tax returns for the last two years (especially if self-employed, commissioned, or a 1099 contractor)

If self-employed: year-to-date profit & loss statement, often two years of business tax returns

Asset Documentation

Last two months of bank statements (checking and savings)

Statements for any retirement or investment accounts you'll use for down payment or reserves

Gift letter and proof of transfer, if part of your down payment is a gift from family

Identification & Credit

Government-issued photo ID

Social Security number (for the credit pull)

Explanation letters for any large deposits, credit inquiries, or past credit issues, if requested

Debt Documentation

Statements for car loans, student loans, credit cards, and any other recurring debt

Current mortgage or lease information if you're currently a renter or homeowner

Employment

Two years of employment history (gaps will need an explanation)

Contact information for verification of employment

Expert Tip: Pull your own credit report before you apply. You can dispute errors before they slow down underwriting, rather than scrambling to fix them mid-transaction.

What Credit Score Do You Need in Katy, TX?

Credit score requirements depend on the loan program, not your city — but here's what applies to Katy buyers using each major loan type:

A higher score doesn't just affect approval odds — it directly affects your interest rate. As of mid-July 2026, average 30-year fixed rates have been running in the mid-6% range nationally, but the rate a specific lender quotes you can vary meaningfully based on credit tier, so shopping multiple lenders matters even more when rates are elevated.

How Does Debt-to-Income Ratio Affect Pre-Approval?

Your debt-to-income (DTI) ratio compares your total monthly debt payments (including the new mortgage) to your gross monthly income.

Two ratios matter:

Front-end ratio: Housing costs alone (principal, interest, taxes, insurance, HOA) — lenders generally like to see this at or below 28–31% of gross income.

Back-end ratio: All debts combined, including the new mortgage — most lenders cap this between 43% and 50%, depending on loan program and automated underwriting results.

Example: If your household earns $8,000/month gross, a lender targeting a 45% back-end DTI would want your total monthly debts — mortgage, car payment, student loans, credit cards, everything — to stay under roughly $3,600/month.

Ways Katy buyers commonly improve DTI before applying:

Pay down or pay off a car loan or high credit card balance

Avoid opening new credit (no new furniture financing or car loans before closing)

Consider a lower-priced target range or larger down payment

Add a co-borrower's income, if applicable

Step-by-Step: How to Get Pre-Approved

Check your credit and gather documents. Pull your credit report and assemble the income/asset documents listed above.

Get quotes from at least two or three lenders. Compare rate, fees, and communication style — not just the headline interest rate.

Submit your application and documents. Most lenders now do this digitally through a secure portal.

Lender runs a hard credit pull and reviews your file. This typically happens within 24–72 hours of a complete file.

Receive your pre-approval letter. This states your approved loan amount, loan type, and any conditions still needed before final "clear to close."

Start house-hunting (or talking to builders) with your letter in hand. Most Katy listing agents and new-home sales reps will ask for it before scheduling a showing or design appointment.

Keep your financial picture stable. No new credit accounts, no job changes, no large undocumented deposits between pre-approval and closing.

Pull Quote: "A pre-approval letter isn't the finish line — it's your starting line. What you do financially between pre-approval and closing matters just as much as what got you approved."

Which Loan Type Is Right for You?

FHA Loans Backed by the Federal Housing Administration, FHA loans allow a 3.5% down payment with a 580+ credit score. For 2026, the Houston-area FHA loan limit (which covers Harris and Fort Bend Counties, including all of Katy) sits at the standard floor of $541,287 for a single-family home. FHA is popular with first-time buyers because of its flexible credit requirements, though it does require mortgage insurance for the life of the loan in most cases.

Conventional Loans Conventional loans can go as low as 3% down for qualified first-time buyers, with better terms generally available at 620+ credit scores. Texas's 2026 conforming loan limit is $832,750, well above most Katy purchase prices, giving conventional financing plenty of room in this market. Put down 20% and you avoid private mortgage insurance (PMI) entirely.

VA Loans For eligible veterans, active-duty service members, and surviving spouses, VA loans offer 0% down with no PMI — a major advantage in a market like Katy, which has a meaningful military and veteran homebuyer population given its proximity to the Energy Corridor and Houston's broader employment base. Mohebbi Realty Group's VA-certified designation means Bobby Mohebbi specifically understands how to structure competitive offers using VA financing.

USDA Loans USDA loans allow 0% down in eligible rural and some suburban-fringe areas. Some outlying communities near Katy — think areas toward Brookshire or Hockley — may fall within USDA-eligible zones, but eligibility is address-specific and should always be verified directly through the USDA's eligibility map before you count on it.

Down Payment Assistance Programs in Texas

Texas has real, statewide down payment assistance that many Katy buyers don't realize they qualify for:

TSAHC Home Sweet Texas Home Loan Program — for low- and moderate-income Texas buyers, offering up to 5% of the loan amount as a grant (no repayment) or a forgivable second lien.

TSAHC Homes for Texas Heroes — the same structure as Home Sweet Texas, but for teachers, firefighters, EMS personnel, police, correctional officers, and veterans.

Mortgage Credit Certificate (MCC) — available to eligible first-time buyers through TSAHC, this is an annual federal tax credit based on mortgage interest paid, not a repayable loan.

To qualify for most TSAHC programs, you'll generally need at least a 620 credit score and to meet income limits that vary by county and household size. These programs can be paired with FHA, VA, USDA, or conventional financing.

Note: down payment assistance program terms, income limits, and available funds change and should always be confirmed directly with TSAHC or a participating lender before you build a budget around them.

How Much House Can You Afford in Katy?

Affordability isn't just about the loan amount you're approved for — it's about what fits your monthly budget comfortably. A few Katy-specific factors to weigh:

Property taxes. Fort Bend and Harris County property tax rates, plus MUD (Municipal Utility District) fees common in many Katy master-planned communities, can add meaningfully to your monthly payment beyond principal and interest. Always ask a lender to run PITI (principal, interest, taxes, insurance) — not just principal and interest — when estimating what you can afford.

HOA dues. Common in Katy's master-planned communities (Cinco Ranch, Cross Creek Ranch, Elyson, Firethorne), these are a fixed monthly or annual cost your DTI calculation should include.

New construction incentives. Many Katy builders offer rate buydowns or closing cost credits when you use their preferred lender — worth comparing against your independent pre-approval to see which nets out better.

How to Choose a Lender in Katy, TX

Not all lenders — or lender relationships — are equal. Here's what to actually compare:

What to compare:

Rate and total fees (APR, not just the headline rate). Ask for a full Loan Estimate, not a verbal quote.

Communication and responsiveness. In a competitive offer situation, a lender who answers your call in an hour beats one who takes two days.

Local market knowledge. A lender who regularly closes loans in Fort Bend and Harris County understands Katy-specific issues like MUD taxes and new-construction draw schedules.

Loan program fit. Not every lender specializes in every program — if you're using a VA loan or a TSAHC down payment assistance program, confirm your lender actually originates those.

Builder-preferred lenders vs. independent lenders. Builder incentives can be valuable, but it's worth getting an independent quote to compare against.

Bobby Mohebbi works with a vetted network of local, Katy-area lenders as part of Mohebbi Realty Group's buyer process — happy to make an introduction if you'd like a starting point rather than shopping cold.

Common Pre-Approval Mistakes to Avoid

Applying with incomplete documents. This is the #1 cause of delayed pre-approvals — missing pages of bank statements or unexplained deposits will stall your file.

Making a big purchase or opening new credit before closing. A new car loan or furniture financing between pre-approval and closing can change your DTI enough to jeopardize your approval.

Changing jobs mid-process. Lenders verify employment again right before closing — a job change, even a good one, can require re-underwriting.

Only getting one quote. Comparing at least two or three lenders is one of the simplest ways to save real money over the life of the loan.

Letting your pre-approval expire. Most letters are valid 60–90 days. If you pause your search, plan to refresh it before you start touring homes again.

Assuming pre-qualification is enough. Especially with Katy builders, confirm specifically that you have a pre-approval, not just a pre-qualification estimate.

Action Items

Pull your credit report and review it for errors

Gather two years of tax returns/W-2s and two months of bank statements

Get quotes from at least two Katy-area lenders

Ask each lender about TSAHC or other down payment assistance eligibility

Confirm your pre-approval letter's expiration date before you start touring homes

Talk to a local REALTOR® about how your pre-approved budget fits current Katy inventory

FAQs

How long does mortgage pre-approval take in Katy, TX? Most lenders can issue a pre-approval letter within 24–72 hours once you've submitted a complete document package. Delays almost always come from missing or incomplete documentation.

Does getting pre-approved hurt my credit score? A hard credit inquiry can cause a small, temporary dip — typically a few points. Multiple mortgage inquiries within a short window (usually 14–45 days, depending on the scoring model) are generally counted as a single inquiry for scoring purposes, which is why it's safe to shop multiple lenders.

Can I get pre-approved with a 580 credit score? Yes — a 580 credit score qualifies for an FHA loan with a 3.5% down payment. Scores between 500–579 can still qualify for FHA but require 10% down. Bobby Mohebbi can help introduce you to credit repair companies also.

How much does it cost to get pre-approved? Pre-approval itself is typically free. You may pay for a credit report pull, but most Katy-area lenders don't charge an upfront fee for pre-approval.

Do I need a pre-approval letter before touring homes in Katy? It's not legally required, but most listing agents and virtually all new-construction builder sales offices in Katy will ask for one before scheduling private showings or lot reservations.

Is pre-approval the same as being approved for a mortgage? No. Pre-approval is a strong, verified estimate based on your documents and credit at that point in time. Final loan approval ("clear to close") happens after the home is under contract, appraised, and your file goes through full underwriting.

What credit score do I need for a conventional loan in Texas? Most lenders want at least a 620 for conventional financing, though better rates and terms typically come with scores of 700+.

SourcesU.S. Department of Housing and Urban Development (HUD) — 2026 FHA loan limit announcementFederal Housing Finance Agency (FHFA) — 2026 conforming loan limitsTexas State Affordable Housing Corporation (TSAHC) — Home Sweet Texas and Homes for Texas Heroes program guidelinesFreddie Mac Primary Mortgage Market Survey — weekly 30-year fixed rate averagesRedfin and Zillow — Katy, TX and 77494 housing market dataConsumer Financial Protection Bureau (CFPB) — mortgage shopping and rate-lock guidanceU.S. Department of Veterans Affairs — VA home loan eligibilityUSDA Rural Development — Single Family Housing Guaranteed Loan Program eligibility

This article reflects program terms, loan limits, and rate data as of July 2026. Loan limits, down payment assistance terms, and mortgage rates change — verify current figures with your lender or the source agency before making financial decisions. This content is for informational purposes and is not a guarantee of loan approval or terms.Written by Bobby Mohebbi — Licensed Texas REALTOR® since 2014, Accredited Buyer's Representative (ABR), Pricing Strategy Advisor (PSA), Short Sales & Foreclosure Resource (SFR), VA-Certified Agent. Founder, Mohebbi Realty Group, Katy, TX.