How to Use 0% Down Payment Programs in Texas (2026 Guide)

Quick answer: You do not need 20% down to buy a home in Texas. Depending on your situation, you may be able to purchase with 0% to 3.5% out of pocket — and in many cases, even that amount can be covered entirely by state and local assistance programs. This guide covers every major Texas homebuyer assistance program available to Greater Houston buyers in Katy, Cypress, The Woodlands, Sugar Land, Pearland, Fulshear, Richmond, Tomball, and Hockley as of June 2026.

The #1 myth in real estate: "I need 20% down to buy a home." Texas has some of the most robust homebuyer assistance programs in the nation, and there is very likely a program that can significantly reduce — or eliminate — your upfront costs.

Program 1: TSAHC — Texas State Affordable Housing Corporation

TSAHC is a nonprofit created by the Texas Legislature. It offers two major programs, both available across the Greater Houston area.

Home Sweet Texas Home Loan Program

Eligibility: All eligible Texas homebuyers (not profession-specific)

Assistance amount: 2%–5% of loan amount

Assistance type: Grant OR forgivable 2nd lien

Minimum credit score: 620

Repeat buyers eligible: Yes

This program pairs a 30-year fixed-rate mortgage (FHA, VA, USDA, or conventional) with assistance that works one of two ways: as a grant that doesn't need to be repaid as long as you don't refinance or pay off the first mortgage within 3 years, or as a forgivable second lien that's forgiven if you stay in the home for 3 years. Income limits apply by county (verify at tsahc.org), a homebuyer education course is required before closing (available online, ~$75–$125), and the home must be your primary residence.

Homes for Texas Heroes Program

Eligibility: Teachers, police, firefighters, EMS, veterans, corrections officers, nurses

Assistance amount: Up to 5% of purchase price

Assistance type: Grant OR forgivable 2nd lien

Minimum credit score: 620

First-time only: No — repeat buyers eligible

Same grant/forgivable structure as Home Sweet Texas. Eligible professions include Pre-K–12 teachers and aides, police officers, firefighters, EMS, corrections officers, veterans, active military, nurses, and allied health professionals. Income and purchase price limits apply by county, and this program can be paired with a Texas Mortgage Credit Certificate (MCC) for additional annual tax savings.

2026 status note: TSAHC's MCC program was relaunched in April 2024 and is currently available only when combined with TSAHC down payment assistance — the standalone MCC remains suspended. Combined with DPA, an MCC provides a 15% annual tax credit on mortgage interest paid.

Program 2: TDHCA — Texas Department of Housing & Community Affairs

TDHCA operates two first-time buyer programs through its Texas Homebuyer Program.

My First Texas Home (MFTH)

Eligibility: First-time homebuyers and qualified veterans only

Assistance amount: Up to 5% of loan amount

Structure: Zero-interest second mortgage, no monthly payment

Minimum credit score: 620

This pairs a 30-year fixed-rate first mortgage at a below-market interest rate with up to 5% of the loan amount in down payment and/or closing cost assistance, structured as a zero-interest, no-monthly-payment second mortgage. It must be repaid when you sell, refinance, or the home stops being your primary residence, and it can be paired with a Texas Mortgage Credit Certificate. Loan options include FHA, VA, USDA, or Fannie Mae HFA Preferred conventional. TDHCA considers anyone who hasn't owned a home as a primary residence in the past 3 years a "first-time buyer."

My Choice Texas Home (MCTH)

Eligibility: Both first-time AND repeat homebuyers

Assistance amount: Up to 5% of loan amount

Structure: Zero-interest second mortgage, no monthly payment

Minimum credit score: 620

Same structure as MFTH, but repeat buyers are eligible — you do not need to be a first-time buyer. Income limits apply (and may differ from MFTH), it's available with FHA, VA, USDA, or conventional loans, and the home must be your primary residence.

Program 3: Texas Mortgage Credit Certificate (MCC)

The MCC is a federal tax credit — not a loan, not a grant — that reduces your actual federal income tax liability every year you own and live in the home.

Annual credit rate: 15% of mortgage interest paid

Maximum credit: $2,000 per year

Duration: Life of the mortgage

Eligibility: First-time buyers; income limits apply

Real example: If you pay $14,000 in mortgage interest in Year 1 and hold an MCC at the 15% rate, you receive a $2,000 tax credit — the annual cap — directly reducing your federal tax bill, not just your taxable income. Over a 30-year mortgage, this can total $60,000+ in tax savings.

2026 status: As of June 2026, TSAHC's standalone MCC product remains suspended, but it's available when combined with TSAHC down payment assistance (15% credit rate). TDHCA's MCC is available through their My First Texas Home Combo program. Always confirm current availability with a participating lender.

Program 4: VA Loan — True 0% Down for Veterans

If you are an active service member, veteran, or surviving spouse, the VA loan is the single best mortgage product available in Texas in 2026.

Down payment: 0% — none required

PMI required: No — none, ever

Loan limit (TX, 2026): $832,750 (full entitlement: no cap)

Minimum credit score: No official minimum; 580+ typical

Zero down payment and no private mortgage insurance alone saves hundreds per month versus FHA. Rates are competitive, often below market rates for FHA/conventional, and with full VA entitlement there's no maximum loan amount and no down payment required, even on a $900,000 home. It can also be combined with Texas state assistance for closing cost coverage, and it's available in every Houston suburb: Katy, Cypress, The Woodlands, Pearland, Fulshear, Richmond, Tomball, and Hockley.

Program 5: USDA Loan — 0% Down in Eligible Areas

The USDA Rural Development loan offers true zero down payment financing for eligible suburban and rural areas. Parts of the Greater Houston outskirts qualify.

Down payment: 0% — none required

Minimum credit score: 620–640

Income limit: ~115% of area median income

Property eligibility: Must be in a USDA-eligible area

Houston-area communities that may have USDA-eligible addresses (verify each specific address):

Parts of Hockley / Waller County

Outer Richmond / Fort Bend County rural portions

Outer Montgomery County (near The Woodlands area but farther out)

Parts of Brazoria County south of Pearland

Katy

Fulshear

Hockley

Conroe

and more suburbs

Always verify USDA property eligibility at eligibility.sc.egov.usda.gov before assuming a specific address qualifies. or Bobby Mohebbi Group can help you identify the areas and homes that qualify for this program.

Program 6: SETH — Southeast Texas Housing Finance Corporation

Program: SETH 5 Star & MyHome Plus

Assistance: Up to 5% of loan amount

Structure: Second loan (not a grant)

Loan types: FHA, VA, USDA, Conventional

SETH programs are available in the Houston area and can be layered with other programs. Ask your lender about current SETH availability and rates, as they change based on market conditions.

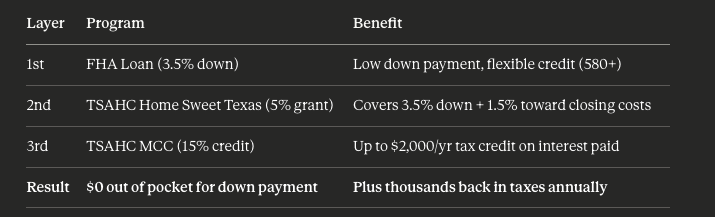

How to Stack Programs for Maximum Benefit

Here's an example of how a first-time buyer in Katy can use multiple programs together:

Real numbers example: On a $350,000 home purchase, a TSAHC 5% grant equals $17,500 — covering your 3.5% FHA down payment ($12,250) plus $5,250 toward closing costs. Combined with an MCC, you also save up to $2,000/year on federal taxes. Total first-year savings: $19,500+. $0 out of pocket!

Funding availability note: Texas DPA programs are funded and can run out of money during peak buying seasons. As of Q4 2025, approximately 82.8% of Texas programs were actively funded (Down Payment Resource Index). Apply early — don't wait until you find a home to start the process. Approval typically takes 30–60 days.

Frequently Asked Questions

Can I use down payment assistance on a new construction home? Yes. Most TSAHC and TDHCA programs can be used on new construction homes, including those from builders like D.R. Horton, Lennar, and Perry Homes in Katy, Cypress, Richmond, and surrounding areas. The builder may offer their own incentives as well, it's worth comparing both options. Bobby Mohebbi can help you identify the best programs for you.

Does the seller know I'm using down payment assistance? Yes, it's disclosed in the contract. Most sellers and listing agents in the Houston area are familiar with DPA programs and don't view them negatively. A pre-approval letter that includes the DPA program makes you a credible buyer.

Can I use DPA on a house that needs repairs? FHA-backed DPA loans require the property to meet FHA Minimum Property Requirements (MPR), and significant repair issues must be resolved before closing. Conventional-backed DPA programs may have more flexibility.

What happens if I sell my home in year 2? For grant-based programs like TSAHC, the grant is yours to keep as long as you don't refinance or pay off the first mortgage within 3 years. For second-lien programs like TDHCA, the second mortgage is repaid from sale proceeds when you sell. always check the information for accuracy

What credit score do I need for Texas down payment assistance? Most TSAHC and TDHCA programs require a minimum credit score of 620. VA loans have no official minimum (most lenders look for 580+), and USDA loans typically require 620–640. If you need help with your credit score, Bobby Mohebbi Group can refer you to a trusted partner to help you with your credit challenges.

Can I combine multiple down payment assistance programs? Yes. A common strategy stacks an FHA loan with a TSAHC grant for the down payment and closing costs, plus a Mortgage Credit Certificate for an ongoing annual tax credit, potentially bringing your out-of-pocket cost to $0. Bobby Mohebbi can help you with securing the best deal that best matches your lifestyle and budget.

About Bobby Mohebbi

Bobby Mohebbi is a Realtor with Keller Williams Signature and leads the Mohebbi Realty Group, helping first-time buyers across Katy, Cypress, The Woodlands, Sugar Land, Pearland, Fulshear, Richmond, Tomball, and Hockley navigate Texas down payment assistance programs alongside the home search and closing process.

This guide is for informational purposes only and does not constitute financial or mortgage advice. Data current as of June 2026. Program details, income limits, funding availability, and terms change regularly — always verify current program specifics with a TSAHC/TDHCA-approved lender before making decisions.Data sources: TSAHC.org 2026 Annual Action Plan, TDHCA.state.tx.us, LendingTree (2026 FHA/USDA limits), Down Payment Resource Q4 2025 Index, Texas Homebuyer Program.

Ready to Find Out Which Programs You Qualify For?

Call or text Bobby Mohebbi today at 832-455-3565 or email Bobby@mohebbirealtygroup.com — I'll connect you with a DPA-approved Houston-area lender who will map out your complete options at absolutely no cost or obligation.